US lithium supply to outstrip electric vehicle demand by 2032: ICCT

The shift towards sustainable mobility will be resource-intensive. Many batteries and battery materials will be needed to supply the growing volumes of BEV sales in the US, and the automotive industry will need to secure a sufficient and affordable supply to manufacture and sell BEVs at prices comparable to their combustion engine counterparts.

A new study by the International Council on Clean Transportation (ICCT), which explores the potential for the United States to secure a reliable supply of lithium, underscores the promising position of the US to meet the challenges of expanding and securing lithium supply for electric vehicles over the next 10 years by comparing announced lithium supply with projected demand.

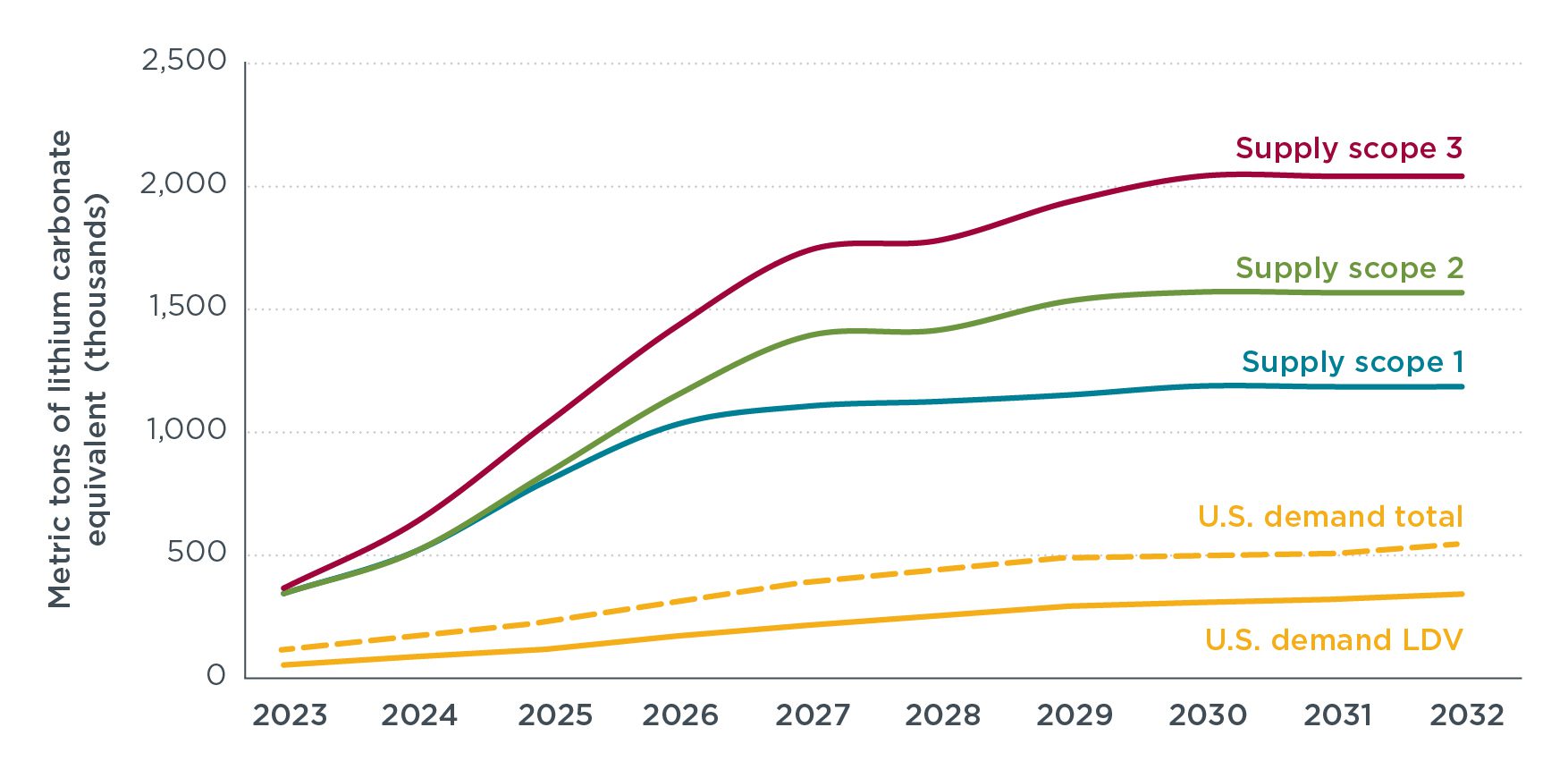

The report finds that by 2032, annual lithium demand from increased sales of light BEVs in the US could rise to around 340,000 metric tonnes per year (ktpa) of lithium carbonate equivalent (LCE). This lithium demand is based on estimates of potential BEV market growth from the EPA's proposed multi-pollutant emissions standards, such that BEV sales shares could increase to 67% of new light-duty vehicle sales in the US by 2032. By identifying three potential scopes for lithium supply, ICCT concludes that new lithium supply can far exceed the lithium demand of new light BEVs in the US through 2032.

The three potential scopes of new lithium supply are based a detailed assessment of new projects within the United State and in countries with which the US has existing or potential future Free Trade Agreements (FTA) or Critical Mineral Agreements (CMA).

“The transition to electric vehicles requires a lot more battery materials, so it’s important that the supply chain keeps pace with EV market growth. The good news is there’s more than 100 lithium mining and refining projects underway within the U.S. and its trade partners” said Chang Shen, Researcher at the ICCT.

The study finds that many dozens of new lithium mining and refining projects are in operation or planned in the United States and its existing and potential future Free Trade Agreements (FTA) and Critical Mineral Agreements (CMA) partners as of 2023. These projects could lead to about 1,200 to about 2,050 ktpa of lithium supply by 2032, or about 3.5 – 6 times higher than the projected lithium needed for new U.S. light-duty BEVs.

The ICCT report also estimates that the United States would account for approximately 17% of this mining capacity and 27% of this refining capacity. Countries with existing FTAs and CMAs like Australia, Canada, Chile, and Peru would account for 56% in mining and 47% in refining capacity. Potential countries for future CMAs, such as Argentina, would account for 28% of mining and 21% of refining capacities considered in this analysis. The study compares potential supply with demand and finds that supply is likely to meet or exceed demand under all supply scopes.

Cost reductions will be needed

The study generates hypothetical price scenarios for three crucial battery materials—lithium, cobalt, and nickel—spanning from 2023 to 2032. It then conducts a comprehensive bottom-up analysis of battery costs to understand how fluctuations in raw material prices influence overall battery pack costs. Consequently, the study evaluates the impact of these battery cost estimates on the pricing of new Battery Electric Vehicles (BEVs) throughout the same period. These analyses reveal two significant findings.

Firstly, the costs of battery packs and BEVs are intricately linked to raw material prices. Despite this correlation, substantial and consistent reductions in both battery and BEV costs are anticipated across various scenarios of raw material pricing.

Secondly, within the United States, IRA aimed at encouraging battery production and BEV purchases are poised to expedite the achievement of price parity by approximately three years.

“Continued battery and electric vehicle cost reductions are needed for widespread consumer adoption. Our research shows a clear path to price parity, and the IRA incentives are making that happen even faster” said Pete Slowik, the ICCT’s U.S. Passenger Vehicles Lead.

Considering announced lithium supply, anticipated cost reductions of batteries, and IRA incentives, the results of the ICCT’s study highlight the promising position of the United States lithium supply to keep up with estimates of potential market growth from EPA’s proposed Multi-Pollutant Emissions Standards while achieving continued expected cost reductions and cost-competitiveness with combustion engine vehicles. This is an encouraging sign for the increased presence of BEVs and the path to a greener future.

Comentarios

Sé el primero en comentar...