European battery production could outshine China with 60% lower carbon emissions

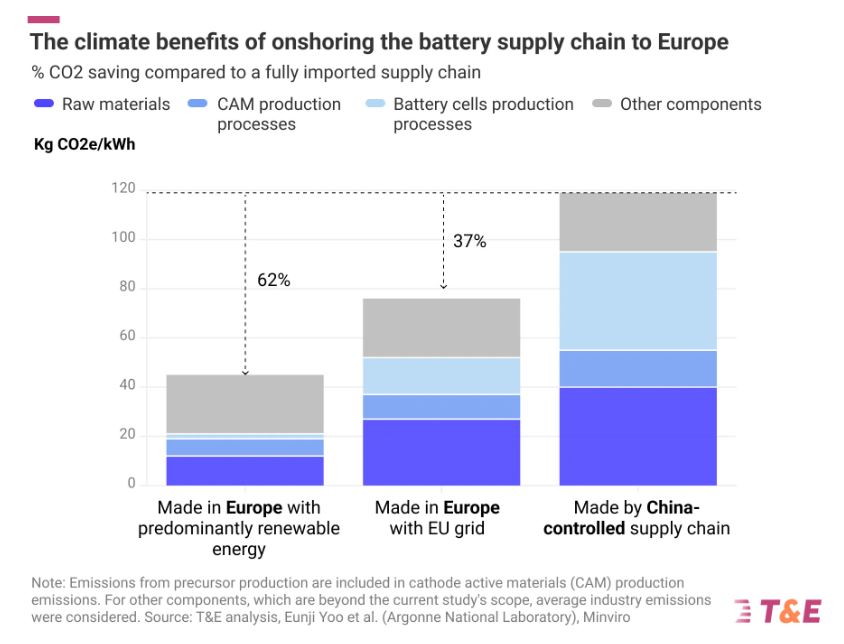

According to a recent analysis by Transport & Environment (T&E), relocating the electric vehicle (EV) supply chain to Europe would result in a 37% reduction in emissions compared to a supply chain controlled by China. This emission reduction increases to over 60% when renewable electricity is utilized. If Europe were to produce battery cells and components domestically to meet its demand, an estimated 133 million metric tons of CO2 emissions could be saved between 2024 and 2030. This figure is equivalent to the total annual emissions of Czechia.

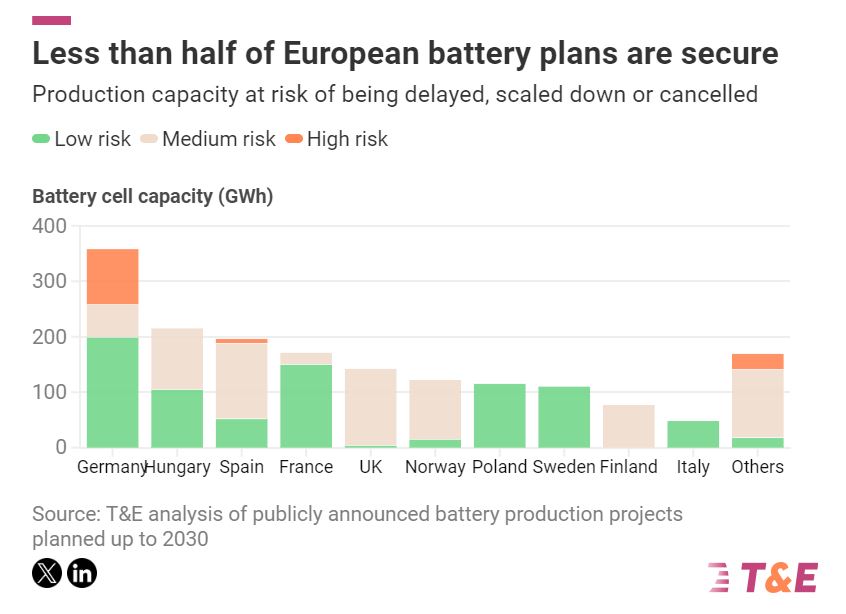

However, the report also discovers that only 47% of the planned lithium-ion battery production for Europe up to 2030 is assured. This represents an increase from one-third a year earlier, thanks to various measures implemented in response to the US Inflation Reduction Act. Nonetheless, the remaining 53% of announced cell manufacturing capacity still faces medium to high risks of being postponed, reduced in scale, or canceled unless stronger government intervention is enacted.

Julia Poliscanova, senior director at T&E, equates the significance of batteries and their metals to that of oil, emphasizing the need for Europe to adopt a precise strategy to leverage climate and industrial benefits. She advocates for stringent sustainability standards, such as upcoming battery carbon footprint regulations, to drive local clean manufacturing. Poliscanova highlights the importance of strengthening mechanisms like the European Investment Bank and EU Battery Fund to boost investments in gigafactories.

She notes escalating battery competition among China, Europe, and the US with some investments preserved despite past risks. However, significant production remains undecided. Poliscanova emphasizes EU clarity on engine phase-outs and corporate EV targets to reassure gigafactory investors of a stable market.

The most significant advancements in securing gigafactory capacity since T&E's prior risk assessment last year have been made by France, Germany and Hungary. In France, ACC initiated production in Pas-de-Calais last year, while plants by Verkor in Dunkirk and Northvolt in Schleswig-Holstein, Germany, are progressing due to substantial government subsidies.

Finland, the UK, Norway and Spain have the majority of production capacity at medium or high risk, primarily due to uncertainties surrounding projects by the Finnish Minerals Group, West Midlands Gigafactory, Freyr, and InoBat. T&E has urged policymakers to facilitate investment assurance by intensifying EU electric car policies, implementing robust battery sustainability requirements that incentivize local manufacturing, and bolstering EU-level funding.

Given China's predominant position and the EU's developing proficiency, securing other segments of the battery value chain will prove to be even more arduous. The report indicates that by 2030, Europe could potentially manufacture 56% of its cathode demand, which represents the battery's most valuable components. However, as of now, only two plants have commenced commercial operations. Additionally, by the end of the decade, the region could satisfy all of its processed lithium requirements and obtain between 8% and 27% of battery minerals through recycling within Europe. Nevertheless, T&E emphasized that processing and recycling facilities require swift scaling, necessitating support from both the EU and member states.

Comentarios

Sé el primero en comentar...