Italy connects 32 GW of solar power by March and adds 1.7 GW in Q1 2024

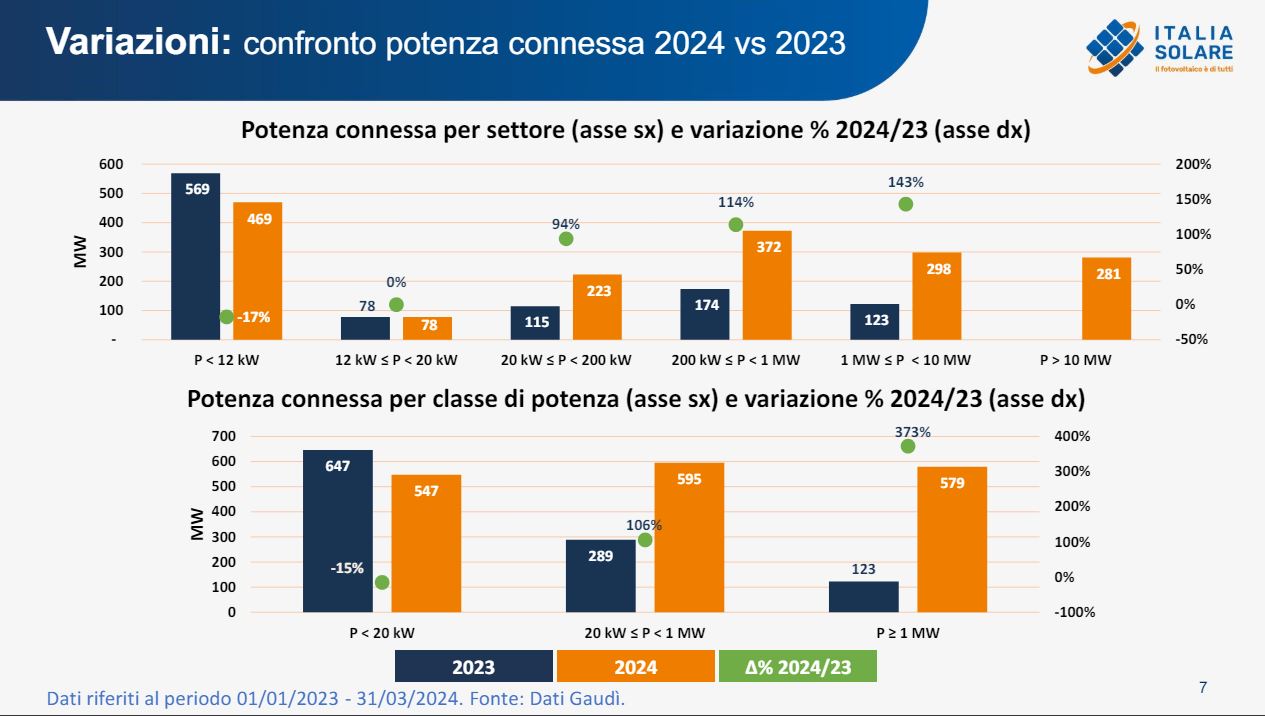

By March 31, 2024, Italy had connected 1,688,348 photovoltaic systems, reaching a total power of 32.00 GW. In the first quarter of 2024 alone, 93,374 new systems were connected, adding 1.72 GW. Of this new power, 32% (547 MW) came from the residential sector (P < 20 kW), 35% (595 MW) from the commercial and industrial (C&I) sector (20 kW ≤ P < 200 kW), and the remaining 34% (579 MW) from utility-scale plants exceeding 1 MW.

Compared to Q1 2023, residential sector power decreased by 15% in the last quarter, while C&I sector power surged by 106%, and utility-scale power skyrocketed by 373%. This significant rise was driven by the connection of eight plants with capacities over 10 MW, totaling 281 MW, in Lombardy (20 MW), Lazio (137 MW), Friuli-Venezia Giulia (24 MW), Sicily (40 MW), Sardinia (50 MW), and Puglia (10 MW). Notably, from October 2023 to March 2024, plants larger than 10 MW were connected monthly, adding up to 622 MW over six months.

Residential sector resilience despite Superbonus conclusion

The residential sector has not seen a significant drop in connections despite the end of the 110% Superbonus, whose completion deadline was extended to December 31, 2023, and the halting of credit transfers. The impact on residential connections is expected to become evident from Q2-Q3 2024. From Q4 2023 (525 MW) to Q1 2024 (547 MW), there was a 4% increase in connected power, and from Q3 2023 (485 MW) to Q4 2023, there was an 8% rise, following a 19% decline from Q2 2023 (602 MW) to Q3 2023.

C&I sector doubles in size over the last year

The C&I sector saw substantial growth in the past year, with connected power in Q1 2024 (595 MW) rising by 106% compared to Q1 2023 (289 MW). This growth was primarily driven by the increase in the PUN (Prezzo Unico Nazionale) in 2022, which only returned to average monthly values below 100 Euro/MWh at the start of 2024. The high energy prices spurred a boom in C&I connections until mid-2023, with the lag between the PUN increase and plant construction attributed to the time required for project commissioning, construction, and connection.

Since the latter half of the previous year, the monthly connected power stabilized in the 150-250 MW range, whereas before the energy crisis, from January 2021 to June 2022, the average monthly connected power in the C&I sector was 38 MW.

As well, utility-scale plants experience a significant surge.Connections of utility-scale plants (capacity > 1 MW) grew by 373% in Q1 2024, with 579 MW connected compared to 123 MW in the same quarter of 2023.

Regional leaders in Q1 2024

Lombardy, Lazio, and Emilia-Romagna were the top regions for new power connections in Q1 2024, with Lombardy connecting 304 MW, Lazio 229 MW, Veneto 188 MW, Emilia-Romagna 150 MW, and Piedmont 131 MW. These regions collectively connected 1 GW, with 27% (274 MW) from the residential sector, 38% (376 MW) from the C&I sector, and 35% (352 MW) from the utility-scale sector.

Compared to the same quarter the previous year, Lazio saw the greatest increase (+373%), followed by Friuli Venezia-Giulia (+185%) and Sardinia (+122%).

Comentarios

Sé el primero en comentar...