US community solar hits 10 GW as installations decline in key markets

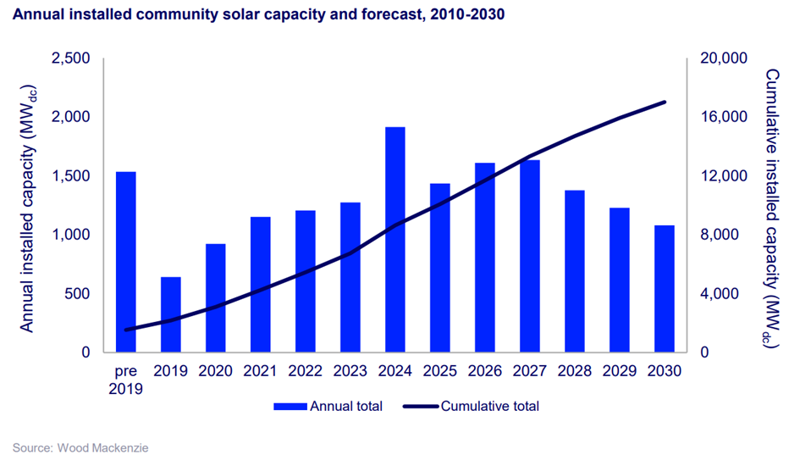

US community solar installations surpassed 10 gigawatts (GWdc) of cumulative capacity at the end of 2025, according to a report by Wood Mackenzie in collaboration with the Coalition for Community Solar Access (CCSA), marking a milestone for the segment despite a broader slowdown in annual deployments.

The report shows that the US market added 1,435 MWdc in 2025, but experienced a 25% contraction in annual installations, driven mainly by weaker activity in mature state markets such as New York and Maine.

Even so, national installed capacity is expected to rebound with 12% growth forecast for 2026, supported by stronger development pipelines and new state-level programs.

“Overall, we expect national installed community solar capacity will contract by an average of 5% annually through 2030 in existing state-level programs,” said Caitlin Connelly, senior analyst and lead author of the report. “The segment’s near-term growth is anchored by a strong project development pipeline that now exceeds 8 GWdc, 29% of which is reported to be under construction. Developers are navigating a complex federal policy landscape and interconnection queue backlogs to ensure their current pipelines are built out as efficiently as possible to meet the start-of-construction and placed-in-service deadlines required to secure the ITC.”

The report also highlights that long-term growth in traditional community solar remains dependent on the expansion of new state markets, with proposed programs in Ohio, Iowa, Pennsylvania and Michigan forming part of early-stage development pipelines.

Wood Mackenzie estimates that new legislation in these markets could add up to 1.5 GWdc through 2030, although the scheduled phase-out of the Investment Tax Credit (ITC) in 2030 is expected to complicate project timelines and design.

At the same time, developers are increasingly shifting toward so-called “community-scale” solar projects, defined as installations of up to 20 MWdc, which are typically connected directly to distribution grids and can be deployed more quickly than larger utility-scale assets. These projects are gaining traction particularly in Ohio and Pennsylvania, where rising electricity demand is driving interest in faster capacity additions, especially when paired with storage.

The report notes that utilities are beginning to incorporate these community-scale resources into long-term planning due to their potential to enhance grid flexibility and reliability.

On the cost side, subscriber acquisition expenses in US community solar declined by an average of 12% in 2025, as developers increasingly adopt digital marketing tools and consolidated billing systems. Wood Mackenzie expects further gradual declines through 2030, although low-to-moderate income (LMI) subscribers remain the most expensive segment, at around $100/kW. The subscription management sector is also undergoing consolidation.

By the end of 2025, four major platforms and vertically integrated developers accounted for approximately 55% of operational community solar capacity, following transactions such as Perch Energy’s acquisition of Solstice and its earlier merger with Arcadia.

Market outlook and scenarios

Looking ahead, Wood Mackenzie outlines a range of scenarios for the market. In a base case, the sector is expected to contract by an average of 5% annually through 2030 in existing state programs.

A high-case scenario projects a 16% uplift, equivalent to around 1.2 GWdc, driven by favorable policy and interconnection reform. A low-case scenario foresees a 14% contraction, or roughly 1 GWdc less capacity, due to stricter tax credit requirements and limited state-level policy support.

Comentarios

Sé el primero en comentar...