US community solar market set to exceed 14 GWdc by 2029

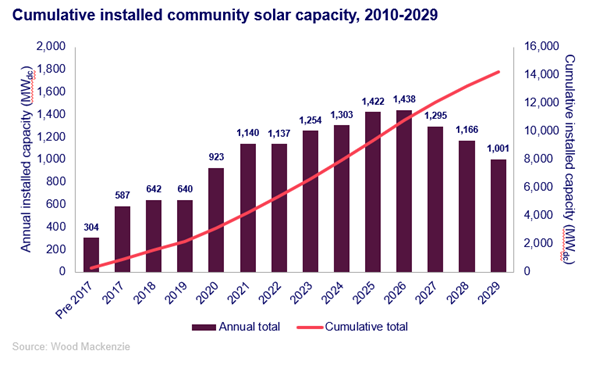

The US community solar market is projected to surpass 14 gigawatts direct current (GWdc) of cumulative capacity by 2029, according to a new report from Wood Mackenzie, in collaboration with the Coalition for Community Solar Access (CCSA). The report highlights that approximately 7.3 GWdc of new community solar installations are expected to come online in existing state markets by the end of the decade.

Challenges for Long-Term Growth

While program pipelines remain robust in mature markets, their ability to sustain long-term growth is limited due to market saturation. Wood Mackenzie forecasts a 5% annual growth rate for the national community solar market through 2026, followed by an 11% average contraction through 2029. Future expansion in program capacity and the emergence of new state markets could potentially offset this decline.

Impact of Recent Policy Decisions

“The US community solar market has tripled in size since 2020, but growth is beginning to decelerate in existing state markets,” said Caitlin Connolly, Senior Research Analyst at Wood Mackenzie. “Additionally, the May 2024 decision on California community solar led to a significant 14% reduction in our five-year national outlook. Long-term growth will largely depend on new state market legislation.”

Source: Wood Mackenzie

Source: Wood Mackenzie

Varied Forecast Scenarios

Under a bullish scenario, Wood Mackenzie’s five-year outlook for existing markets could increase by 21% compared to the base case. Conversely, a bearish scenario predicts a 20% decrease. These scenarios do not factor in the potential impact of new state markets, such as Ohio, Pennsylvania, Michigan, and Wisconsin, which have shown significant interest and pre-development activity.

Legislative Impact on Market Outlook

Wood Mackenzie estimates that if proposed legislation in Ohio, Pennsylvania, Michigan, Wisconsin, and other potential states is enacted, the national outlook could see at least a 17% uplift from the base case. In a bullish scenario with successful legislation, the cumulative national capacity could reach 17.1 GWdc by 2029.

Navigating Federal Incentives

Community solar developers are also adjusting to federal incentives. “The benefits of the Inflation Reduction Act are substantial but challenging to quantify,” said Connolly. “Developers are navigating a steep learning curve while seeking tax credit adders. The $7 billion ‘Solar for All’ fund, announced in April 2024, offers additional opportunities, though final implementation plans are still pending.”

Increased Focus on Low-to-Moderate Income (LMI) Subscribers

The report indicates that 3.6 GWdc of community solar will serve low-to-moderate income (LMI) subscribers by 2029. Currently, 829 MWdc of community solar directly benefits LMI subscribers, with this share growing from 2% in late 2022 to 12% in early 2024. The share dedicated to LMI subscribers is expected to reach nearly 25% by 2025.

Industry Insights

“One of community solar’s unique benefits is its ability to provide significant bill savings to small businesses and working families,” said Jeff Cramer, CEO of CCSA. “We’re on track to meet our goal of delivering 4 GWdc of dedicated capacity to low-income residents by 2030 and are optimistic about the positive impact of Solar for All.”

Cost of Subscriber Acquisition

The top three subscriber management companies handle 56% of total community solar subscribers and 71% of LMI subscribers. The report notes that LMI subscriber acquisition is more costly, averaging $113 per kilowatt, which is 27% higher than the cost for non-LMI residential subscribers. Outsourcing subscriber management to third-party firms can help developers reduce these costs.

Comentarios

Sé el primero en comentar...